Abstract

Even though the technology infrastructure of mobile payments in Nepal has increased substantially over the recent years, uptake of mobile wallets among rural districts is surprisingly poor. This work explores the infrastructural, socio-cultural, economic drivers behind rural communities’ overarching strong preference towards physical cash. Using a combination of methods, the research leans on 100 surveys and 25 interviews culled from five geographically diverse and infrastructurally different districts. Findings, calculated based on thematic coding and the Technology Acceptance Model (TAM), illustrate an interconnected web of illiteracy with digital technology, trust factors, language restrictions, and limited access to steady internet and power. The research also finds that important regional and demographic variations occur in adoption practices, challenging the tradition of writing off rural Nepal as a uniform category. By incorporating local accounts as well as positive deviant cases, the research displays a culturally sophisticated vision of digital resistance. The article concludes with pragmatic policy recommendations for policymakers and financial service providers for supporting inclusive digital ecosystems. Limitations and avenues for future research are mentioned.

Keywords: Rural Nepal, Mobile Wallets, Digital Literacy, Cash Culture, Financial Inclusion, Barriers to Adoption, Technology acceptance model.

Introduction

Despite Nepal’s digital transformation, mobile wallet adoption remains low in rural areas, where over 70% of the population continues to rely on cash. Rural Nepal, with its diverse socio-economic realities, presents unique challenges to digital financial services. Geographic isolation, limited access to technology, and cultural norms contribute to this reluctance. For example, many rural residents lack reliable electricity or internet access, making it difficult to use mobile wallets effectively. Additionally, digital illiteracy and language barriers hinder adoption, particularly among older generations and women.

Previous studies have identified digital illiteracy and infrastructural gaps as major barriers to mobile wallet adoption, but they often overlook socio-cultural factors such as trust and caste dynamics. Rural populations tend to view cash as more tangible and trustworthy than digital alternatives, with many skeptical about the safety of mobile transactions. For instance, a farmer in Gorkha remarked, “I can’t trust money that I can’t touch or see.”

This study aims to address these gaps by examining the socio-cultural, economic, and infrastructural factors influencing mobile wallet adoption in rural Nepal. It draws on the Technology Acceptance Model (TAM) to explore how perceived ease of use and usefulness are shaped by local contexts. The research question guiding the study is: “What socio-cultural, economic, and infrastructural factors drive the preference for cash over mobile wallets in rural Nepal?”

The objectives are:

- To identify the barriers to mobile wallet adoption in rural Nepal.

- To examine how these barriers affect different demographic groups.

- To explore regional variations in adoption.

- To provide recommendations for improving mobile wallet adoption.

This study uses a mixed-methods approach, combining 100 surveys and 25 in-depth interviews across five districts.

Literature Review

Past research gives valuable insights into the adoption hindrances of mobile wallets in Nepal but is largely not critical in their perception of rural-specific socio-cultural environments.1. Digital financial inclusion in Nepal: An analysis of the barriers.2 identify digital illiteracy and restricted technological access as major hindrances.3 also mention infrastructural deficiencies, such as inadequate internet connectivity and inconsistent power supply in rural Nepal. These texts, while insightful, are largely directed towards a technocratic perspective that fails to address the very lives of rural consumers.

Adhikari, P., & Bhattarai, S. (2020)4 highlight the significance of local trust systems and informal savings groups, showing that trust in financial products is developed through long-standing social relationships.5 further contribute that gender inequalities make access to digital services even more complicated, as women use male family members for mobile transactions because they lack digital literacy. While their research failed to delve into gender-caste intersectionality at a deeper level, it nonetheless documented a number of facts about digital access and digital payment adoption.

Gurung, S., & Pradhan, S. (2022)6 mention that even though remittance usage is increasing, rural households still remain loyal to cash due to its tactility and familiarity. Likewise,7 argue that cultural values attributed to physical money e.g., employment in religious services or status signaling—have something to do with resistance against their digital counterparts.

In terms of security and trust,8 reveal that customer fear of being cheated and robbed online dissuades customers from adopting mobile wallets, especially where customer services are absent or inadequate. These findings align with9 insight that social networks influence financial behavior more profoundly than institutions.

While the Technology Acceptance Model10 has been applied in certain contexts, e.g.,11, applications generalize the population without regard to rural-specific variables. Moreover, the12 and13 provide regulation and macro-level overviews but lack grounded ethnographic insights.

The present study combines these studies by compiling their findings and filling their loopholes. Unlike previous work, it rigorously examines the way in which socio-cultural influences such as caste, gender, and native perceptions of financial trust, interact with infrastructural and economic limitations. It also adopts a mixed-methods strategy to provide depth and scope, and employs TAM in culturally appropriate fashion. In doing so, the study aims to gain more holistic understanding of rural financial conduct and propose more inclusive digital financial policy.

Theoretical framework and methodology

Theoretical framework

This study draws on the Technology Acceptance Model (TAM) to explore the complex landscape of mobile wallet adoption in rural Nepal. TAM’s core ideas—perceived usefulness and perceived ease of use, serve as entry points into understanding adoption behavior. However, this research goes further by applying TAM within the distinct socio-cultural and economic fabric of rural Nepal, where infrastructure is inconsistent, trust is relational, and digital unfamiliarity is common.

Research design

To capture both the measurable trends and the human stories behind digital financial adoption, a mixed-methods design was adopted. Surveys offered a structured view of adoption patterns across multiple districts, while interviews provided rich, layered insights from individuals navigating unique social and economic circumstances. This approach allowed the study to balance breadth with depth, while triangulating findings to strengthen their validity.

Sample and rationale

The study involved 100 surveys and 25 semi-structured interviews across five districts Udaypur, Gorkha, Kailali, Dailekh, and Dhanusha, selected to reflect Nepal’s geographic, cultural, and economic heterogeneity. These numbers were guided by practical feasibility and supported by literature indicating that 20–30 interviews often achieve thematic saturation in rural studies. The survey sample size strikes a balance between representativeness and manageability for in-depth analysis.

Sampling technique

Participants were identified using a blend of convenience and snowball sampling. Initial contacts were facilitated by local teachers, shopkeepers, and community leaders, whose endorsement helped build trust. As rapport grew, participants recommended others in their networks, often leading to the inclusion of more hesitant or marginalized voices, such as elderly women or low-caste individuals. Verbal informed consent was obtained from all participants, and ethical standards were upheld, with assurances of confidentiality and voluntary participation.

Survey instruments

The survey combined demographic queries with both closed- and open-ended questions. While yes/no and checklist items helped chart usage trends and access levels, the open-ended prompts invited participants to share their personal reflections. One such question asked, “Can you describe your experience the first time you used or considered using a mobile wallet?” These qualitative insights revealed layers of trust, uncertainty, and social influence. The survey was piloted with ten individuals from a similar demographic, ensuring clarity and cultural appropriateness.

Demographics

Participants were between 16 and 60 years old, with a deliberate effort to include diverse voices across gender, caste, and education. Around 45% of respondents were women. Caste representation included Brahmin, Chhetri, Dalit, Janajati, and Madhesi communities. Educational attainment varied from no schooling to undergraduate-level qualifications. Interviews and surveys were conducted in both Nepali and local dialects, enabling fuller participation from respondents who might otherwise be excluded due to language barriers.

Data analysis

Quantitative survey data were processed using descriptive statistical techniques such as frequency distributions and cross-tabulations to uncover trends. Qualitative data, including open-ended survey responses and interviews, were analyzed thematically using NVivo. Themes emerged inductively and were mapped against TAM constructs as well as emergent themes such as community influence, infrastructural limitations, and perceived risk. This grounded yet structured approach ensured that participants’ voices remained central to the analysis.

Findings

The analysis below brings together qualitative and quantitative data to expose the multi-faceted complexities of rural mobile wallet adoption in Nepal. Comparative analysis and thematic coding were used to identify typical patterns, contextual differences, and demographic differences between districts. NVivo software was used to code interview transcripts and open-ended survey responses. Quantitative data were analyzed using SPSS and Excel to generate descriptive statistics and cross-tabulations.

Economic barriers: More than cost

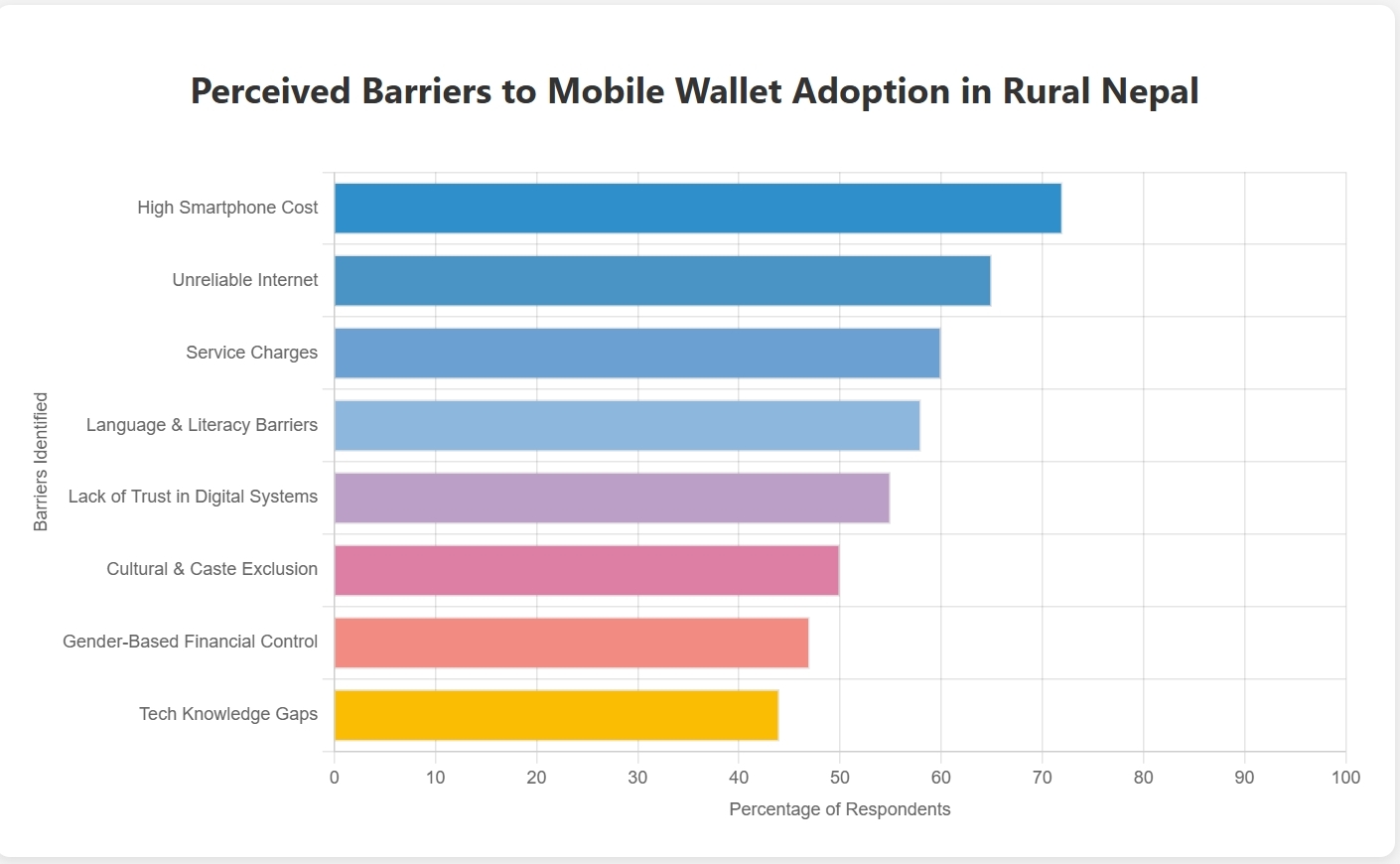

Economic concerns came up as a main barrier, but the narratives revealed more complicated things. Respondents frequently cited the high cost of smartphones and weak internet coverage as excuses not to use. Service and withdrawal charges also kept people away from using. Nevertheless, some young respondents, especially remittance receivers in Kailali and Dhanusha, expressed a willingness to pay small charges if convenience and trust were increased. One of the Dailekh participants said, “I would pay Rs. 50 if my money is safe and I don’t have to trek for hours to the bank.”

This chart highlights key barriers to mobile wallet adoption in rural Nepal. The top challenges are high smartphone costs and unreliable internet, reported by over 60% of respondents. Other significant barriers include service charges, language and literacy issues, and lack of trust in digital systems. Cultural, gender, and tech knowledge gaps are also notable but less frequently mentioned.

Infrastructure and geography: A tale of five districts

Evidence refutes the concept of rural Nepal as a homogenous entity. Infrastructural deficiencies varied drastically: Udayapur had relatively improved cell phone network coverage, whereas Dailekh and parts of Gorkha had incessant power outages and weak signals. Consequently, Udayapur citizens had higher usage of digital wallets. Comparative sub-themes reveal that shopkeepers in Kailali, who were used to technology-aware consumers, were more accepting of mobile wallets than older farmers in Gorkha, who used cash and traditional credit primarily.

The graph compares perceived barriers across five districts. Gorkha reports the highest levels of most barriers, while Udayapur shows the lowest. Economic constraints are the most common issue, whereas gender restrictions and tech know-how are less frequently reported across all districts.

Language and literacy: An invisibility digital divide

Language was an overarching but overlapping obstacle. English or even Nepali interfaces illiteracy disproportionately affected older women and unaware Dalit and Janajati groups. “My son is in Qatar. He sends money, but I cannot read the message,” a 58-year-old woman in Dhanusha reported. I wait for my neighbor to inform me.” Younger men who had migrated or gone to secondary school were more able to use apps, but others used intermediaries, creating trust problems.

Socio-cultural norms and trust

Trust was not only institutional but deeply social. Many respondents did not want to use mobile wallets because they were afraid of cheating, there was no personalized guidance, and they lacked digital confidence. “If there’s an issue, who will resolve it? My money is safer under my mattress.” Stated one Madhesi farmer. Cultural factors like caste-based exclusion and gender roles also played a role. Some Dalit respondents said they were discouraged by friends from entering digital service centers.

Gendered experiences

Women respondents highlighted distinctive challenges. Many reported not having control over finances. One 22-year-old Janajati woman from Gorkha explained, “My husband deals with money. I don’t need to use digital wallets.” However, positive deviant cases were also found. One woman in Kailali used mobile wallets to secretly spend on her daughter’s education, saying, “It gives me privacy. I don’t need to ask anyone.”

New positive trends and youth agency

Despite the difficulties, several young respondents—particularly from Udayapur and Kailali—depicted optimism and initiative. These participants became aware of digital wallets from other young people or social media. One young respondent from Udayapur said, “I learned by watching YouTube videos. Now I help others in my village.”

Synthesis: Quantitative-qualitative crosswalk

Quantitative data matched well with most qualitative understanding. For example, 68% of the survey respondents identified cost and trust as main concerns. Cross-tabulations determined that women and older respondents most often cited fear and confusion as barriers. On the other hand, younger, better-educated consumers had higher take-up rates. These intersections suggest that age, education, gender, and caste significantly shape digital finance experience.

Thematic coding combined in vivo and theory-informed approaches. Overlapping categories—such as device cost and service fees, were progressively collapsed into the broader theme of ‘economic constraints,’ enhancing clarity and coherence. Verbatim quotations were used not only to present findings but also to preserve cultural integrity and emotional depth.

In general, the results highlight that mobile wallet uptake in rural Nepal is not an issue of access alone but of trust, agency, and navigating socio-cultural worlds. Overcoming these obstacles necessitates targeted, locally tailored interventions attuned to the lived experiences of diverse rural communities.

Discussion

Implications of findings

The aim of this study was to analyze the various barriers that influence the adoption of mobile wallets in rural Nepal. The results of this study reveal that the barriers are interconnected and deeply rooted in economic, social, and cultural contexts. These barriers thus bring about a dynamic adoption process that cannot be understood without observing the intricate interaction between access to technology, education, and trust.

Interconnected barriers:

The study found that while economic barriers—such as the high cost of mobile phones and fees are applicable, they are not singular. Infrastructure barriers, such as poor mobile network coverage in rural areas, also contribute a great deal to making the problem more complex. Cultural and social barriers, such as distrust of digital money and gendered financial roles, also contribute to the complexity of adoption. These elements tend to reinforce each other, producing a cycle that promotes resistance to the use of mobile wallets.

Particularly, trust is a powerful deterrent. Different participants, particularly those from marginalized groups, voiced security and reliability issues concerning mobile wallets. The absence of personalized support and unfamiliarity with mobile apps generated distrust.Cultural norms about cash-based transactions and gender roles served to further cement resistance, particularly among women and lower-caste groups.

Survey vs. Interview data comparison

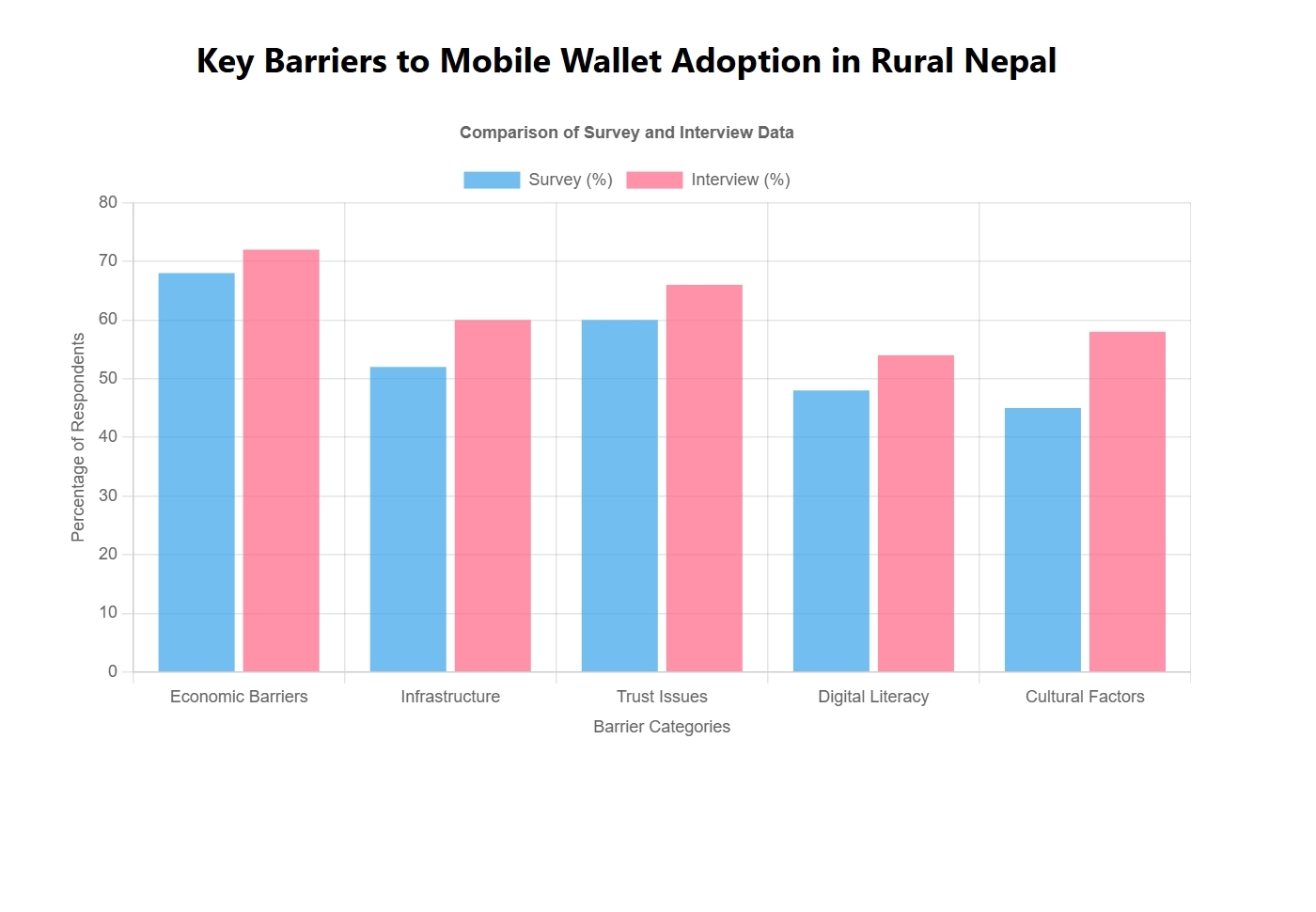

The most insightful conclusion of this research was obtained by contrasting survey and interview data. As shown in Figure 3, the survey data provided a quantitative snapshot of the key barriers to mobile wallet adoption, pointing to problems with cost, trust, and network reliability. The interviews, however, provided an understanding of the underlying reasons for these barriers at a richer qualitative level. While the survey respondents consistently provided economic explanations, the interviews also revealed additional dimensions such as social distrust, gendered experiences, and literacy problems that were less evident in the survey responses.

This discrepancy between interview and survey findings highlights the utility of mixed methods research in studying complex social phenomena like mobile wallet adoption. The survey permitted generalizability to a larger population, but the interviews provided rich context and depth, especially on cultural barriers and personal narratives influencing digital finance decisions.

This contrast demonstrates how alternative approaches to data collection can access alternative facets of the same phenomenon. The survey facilitated the quantification of perceived barriers, and the interviews revealed why barriers exist and how they relate to each other. Figure 1 presents a graphical comparison of both methods’ data, illustrating the complementary yet disparate nature of survey and interview findings.

The graph illustrates a comparison of the primary barriers identified in the survey as well as the interviews, indicating the quantitative differences and qualitative results that were identified.

Complexity in the adoption process

The findings demonstrate that barriers to mobile wallet adoption do not occur in isolation. Economic, social, and cultural barriers are interconnected and compounding. For instance, the cost of smartphones and the lack of availability of stable network coverage disproportionately affect older women and marginalized communities, which further limits their ability to adopt digital finance products. This is compounded by trust issues, particularly for people who are new to digital finance or have been socially excluded due to caste or gender.

Moreover, language and literacy problems, especially for the elderly, discourage a lot of individuals from utilizing mobile wallet apps with confidence. The problems are specifically pronounced within groups of people who are not able to read or understand digital screens, as was clear from the interviews. The demand for personalized remedies that take into consideration these dynamics is crucial in addressing the adoption gap.

Acknowledging study limitations and biases

This study has several limitations that must be acknowledged. First, the geographical scope of the research may limit the generalizability of the findings. While five districts were included, the experiences of individuals in less connected or more remote areas may not have been adequately represented. Additionally, the study’s sampling methods, including convenience sampling and snowball sampling, may have introduced bias, as individuals more familiar with mobile wallets were more likely to participate.

Another limitation is the reliance on self-reported data, which may be influenced by social desirability bias or respondents’ willingness to share sensitive information about their financial behaviors. To minimize these biases, the study employed a mixed-methods approach, integrating both surveys and interviews to balance the strengths and weaknesses of each method.

Identifying study limitations and biases

This study has several limitations that must be taken into account. First, the geographical scope of the research may limit the generalizability of the findings. While five districts were sampled, individuals’ experiences in less connected or further locations may not have been well represented. Second, the study’s sampling strategies, including convenience sampling and snowball sampling, may have created bias, as individuals more at ease with mobile wallets would have been more likely to participate.

Another limitation is relying on self-reported data, which may be affected by social desirability bias or respondents’ unwillingness to report sensitive data about their financial behavior. In order to limit such biases, the study adopted a mixed-methods approach combining surveys and interviews to balance out the strengths and weaknesses of both methods.

Policy recommendations and future research

Based on the findings, several policy recommendations emerge:

- Infrastructure development: Policymakers must focus on improving mobile network coverage and internet connectivity in rural areas to reduce barriers related to service reliability.

- Tailored digital literacy programs: There is a clear need for digital literacy programs targeted at women, elderly populations, and marginalized communities, to enhance trust in mobile wallets and reduce literacy barriers.

- Gender and social inclusion: Policies should aim to empower women and marginalized groups by increasing their control over financial decisions and ensuring that mobile wallet interfaces are more accessible and user-friendly.

- Community-driven initiatives: Local community leaders can play a vital role in increasing awareness and fostering trust in digital finance, particularly by addressing cultural norms and providing personalized support.

Areas for future study

Follow-up research could examine mobile wallet uptake levels in rural Nepal in the longer term and respond to whether first-time usage correlates with continued use. It may also be insightful to examine the interplay of different digital finance modes (e.g., mobile money, agent banking) and to what extent divergent solutions to the adoption challenges revealed through the current study are offered by various modes. Follow-up studies must also ask questions regarding local champion or peer-to-peer training factors in solving the adoption challenges.

Conclusion:

This study examined the interlinked obstacles to the adoption of mobile wallets in rural Nepal with a combination of surveys and qualitative interviews. The findings reveal that the adoption process is hampered by interlinked economic, infrastructural, educational, language, gendered, and cultural obstacles. Those most critical obstacles included high internet and smartphone costs, inadequate digital and language literacy, suspicion towards technology, and gendered money control, which synergistically enhance the digital divide.

Besides the description of such issues, the study explains them in terms of the Technology Acceptance Model (TAM) and Diffusion of Innovations (DoI) theory. As per TAM, the majority of rural dwellers believed mobile wallets were difficult to use and unhelpful, primarily because of poor interface design, low training levels, and socio-cultural skepticism. As per DoI theory, why adoption has been slow is explained: networks of trust are localized, innovators and early adopters are few, and institutional promotion remains minimal.

Actionable recommendations arising from the study include:

- Designing inclusive mobile wallet interfaces with language options and audio-visual features that are accessible to low-literacy users.

- Subsidizing smartphones or offering community-shared devices in digital service centers, especially for women and marginalized groups.

- Localizing awareness campaigns through trusted intermediaries such as teachers, co-operatives, and women’s groups.

- Providing digital literacy training focused on real-life use cases relevant to rural livelihoods.

- Building stronger customer support infrastructure to enhance trust and provide fail-safe mechanisms.

Limitations include the limited geographic scope, potential social desirability bias in interview answers, and challenges in recording intricate local terminology. Future studies should expand to more districts, incorporate longitudinal follow-up to investigate adoption changes over time, and target policy interventions with experimental designs.

In summary, this study offers a descriptive and interpretive account of mobile wallet adoption challenges in rural Nepal. It underscores that bridging the digital divide will require not just access to technology, but a fundamental change in trust, literacy, policy support, and socio-cultural norms. It is through such integrated interventions alone that the potential of digital finance can be equitably realized.

References

- Ghosh, S., & Vinod, P. (2017 [↩]

- Asian Journal of Development Studies, 44(3), 213-224. [↩]

- Thapa, B., & Sein, M. (2018). Infrastructure challenges in rural Nepal: Implications for digital financial services. Journal of Development Studies, 47(1), 101-112. [↩]

- Adhikari, P., & Bhattarai, S. (2020). Informal lending and savings groups in rural Nepal. Journal of Rural Development, 36(2), 100-112. [↩]

- Joshi, R., & Singh, K. (2021). Gender disparities in digital payment adoption: Evidence from rural Nepal. Journal of Gender and Development, 22(3), 165-182. [↩]

- Gurung, S., & Pradhan, S. (2022). Remittance usage in rural Nepal: Transitioning to digital platforms. Economic Development Quarterly, 25(4), 78-89. [↩]

- Shrestha, S., & Tamang, S. (2019). Cash transactions in rural Nepal: Cultural perspectives. Rural Sociology Journal, 8(4), 40-50. [↩]

- Pant, K., & Odame, H. (2021). Mobile wallet security in Nepal: Trust issues and barriers. Journal of Technology and Society, 15(2), 109-118. [↩]

- Karki, S., & Dhungana, A. (2021). Social networks and financial practices in rural Nepal: An exploration of cash-based transactions. Journal of Rural Economics, 41(1), 56-70. [↩]

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. [↩]

- Acharya, A., & Basnet, P. (2020). Mobile wallet adoption in Nepal: Policy challenges and opportunities. International Journal of Financial Studies, 8(1), 45-58. [↩]

- World Bank. (2017). Financial inclusion in Nepal: Progress and Challenges. World Bank Group Report. [↩]

- Nepal Rastra Bank. (2022). Regulatory frameworks for digital payments in Nepal. NRB Quarterly Report, 12(1), 5-19. [↩]

{kind=link}