Abstract

Entrepreneurship is widely recognized as a key mechanism to alleviate Indigenous disadvantage, yet Indigenous-owned businesses in Canada demonstrate persistently worse survivability, performance, productivity, and formation metrics. This study proposes limited access to business debt financing as a potential critical factor associated with these disparities. A narrative literature review of peer-reviewed and grey literature published (2010-2025) was conducted. The findings were organized and synthesized using narrative synthesis to illustrate how the proposed mechanism of limited access to business financing is linked to the adverse business outcomes and the major barriers associated with this state of lower access to business debt financing for Indigenous-owned businesses. The evidence, first, reveals Indigenous-owned businesses see lower business outcomes—disparities that persist even after controlling for poverty and rurality. Second, the review identified the specific pathways in which limited access to financing is associated with lower business survivability, performance, innovation, and formation among Indigenous businesses—for example, financing exclusion correlates with liquidity constraints and lower firm survival rates. Third, the review identified the institutional, situational, social, and socioeconomic barriers associated with Indigenous entrepreneurs’ reduced access to business debt financing, reflected in lower loan approval rates and reduced credit usage. Entrepreneurship is associated with broader economic outcomes, where securing business financing is related to whether Indigenous ventures can expand employment or contribute to poverty alleviation. Addressing these barriers to capital is therefore essential to unlocking the entrepreneurial capacity of Indigenous communities and lessening disadvantage. Future research should focus on improving data collection and creating policy interventions.

Keywords: Indigenous peoples, entrepreneurship, business financing, economic development, Canada, financing exclusion

Introduction

Canada is a developed country with a highly advanced economy, but its Indigenous population experiences markedly lower socioeconomic status than their non-indigenous counterparts1. In recent decades, the establishment, management, and expansion of Indigenous businesses has been recognized as a primary method in closing the socioeconomic gap between Indigenous and non-Indigenous people because of its ability to facilitate job creation2‘3. However, the literature reveals a pattern of how Indigenous-owned businesses experienced worse business outcomes relative to non-Indigenous-owned businesses—where this disparity exists even after controlling for confounding variables such as rurality or poverty. The central thesis of this paper is the proposition that limited access to business financing is a potential mechanism associated with these disparities.

Yet, the literature is fragmented. On one hand, studies analyzing the association between exclusion from financing and Indigenous business outcomes usually highlight a single pathway, rather than mapping the full range of pathways through which financing exclusion may be linked to Indigenous businesses’ business outcomes. One example of this literature gap Cooper3, who identified one key challenge Indigenous entrepreneurs face in Canada in starting and maintaining a business venture: limited funding or access to capital; however, his analysis focuses almost exclusively on how constrained financing capacity is associated with limited ability to get ventures off the ground and operating, rather than providing a comparably detailed examination of other points in the business cycle through which financing exclusion may influence broader business outcomes. Similarly, Schembri4 identified how Indigenous firms’ ability to innovate is lower in contexts characterized by a certain lack of capital, yet his discussion does not substantially extend to how financing constraints are associated with the other stages of business development or performance. This review seeks to fill this gap by presenting a more unified account of the associations financing exclusion may have with Indigenous businesses’ outcomes. In doing so, this paper seeks to answer the research question: How does limited access to business financing relate to business outcomes of Indigenous entrepreneurs and businesses in Canada? This research question is then translated into two research objectives: (1) document the specific pathways through which limited ability to access business financing is associated with the business outcome disparities between Indigenous and non-Indigenous businesses across survival, performance, productivity, and formation, and (2) identify the major barriers associated with Indigenous entrepreneurs’ reduced financing access. To fulfill these research objectives, this study will draw on peer-reviewed and recognized grey literature published between 2010 and 2025, focusing on Indigenous peoples in Canada, where the literature will then be synthesized using narrative synthesis. The impact of this research is that it provides Canada’s policymakers clearer evidence and a more comprehensive understanding of the pathways of financing exclusion associated with worse business outcomes, enabling policymakers to design more effective policies rather than devising policies based on incomplete information.

This study examines Canada’s Indigenous population, encompassing First Nations, Métis, and Inuit entrepreneurs and businesses. Its scope is limited to one financial domain of business debt financing and one outcome domain of business outcomes. The limitation of this review is that because most evidence is cross-sectional and data is limited, the review cannot establish causation. However, given the scarcity of Indigenous economic data in Canada, this analysis reflects what can be drawn from the evidence currently accessible; nonetheless, findings should be interpreted as identifying relationships that require further longitudinal investigation to establish definitive causation. Additionally, as stated before in this introduction, the thesis of this paper is that limited access to business financing constitutes a potential mechanism associated with business disparities. Indeed, other explanations certainly exist; however, this study confines its analytical scope to financing constraints. This intentional narrowing is adopted not only to maintain coherence with the research’s stated thesis but also to ensure that the scope remains manageable for a single research study.

Method

This study uses a literature review design with narrative synthesis as its method of synthesis. Limited access to business financing is defined as when access to business financing is inhibited, insufficient, or unequal. The association with business outcomes is examined when business outcomes such as formation, growth, survival, innovation, and productivity see lower levels. Indigenous people is used as an umbrella term encompassing the Métis, First Nation, and Inuit5. And, unless explicitly specified otherwise, the terms Indigenous people and Indigenous entrepreneur refer to both on-reserve and off-reserve populations. The term Indigenous communities refers only to recognized Indigenous reserves, and geographic distinctions are made only when the analysis applies exclusively to one group. Furthermore, unless explicitly specified otherwise, the term Indigenous business encompasses both on- and off-reserve businesses. Business debt financing is one of the main methods businesses use to raise capital. In debt financing, a business borrows money from a bank, credit union, or private lender, with the agreement to repay that money with interest6.

This research searched the databases JSTOR, EBSCO, ProQuest, and Web of Science. Search terms combine identifiers of Canada’s Indigenous populations with financing concepts and business outcomes. Boolean operators were then used to create more targeted queries. The review is limited to works published between 2010 and 2025. The justification for this extended timeframe is due to the lack of contemporary, granular data on Indigenous economies in Canada. The inclusion of studies is evaluated on three criteria: the study focuses on the Indigenous people of Canada; the study examines Indigenous people’s barriers to accessing business debt financing; linkage of financing conditions to at least one business outcome. Studies ideally meet all three criteria, or at least two criteria combinations. Both qualitative and quantitative research are eligible, as well as mixed-methods work. Relevant grey literature was also included.

The review uses narrative synthesis as described by Popay et al.7. Specifically, the review applies the following four elements of Popay et al.’s framework: developing a theoretical framework, developing a preliminary synthesis, exploring relationships within studies, and assessing the robustness of the synthesis. In the spirit of providing a more transparent methodology, each element of Popay et al.’s will be explained in depth on how it was applied to this review.

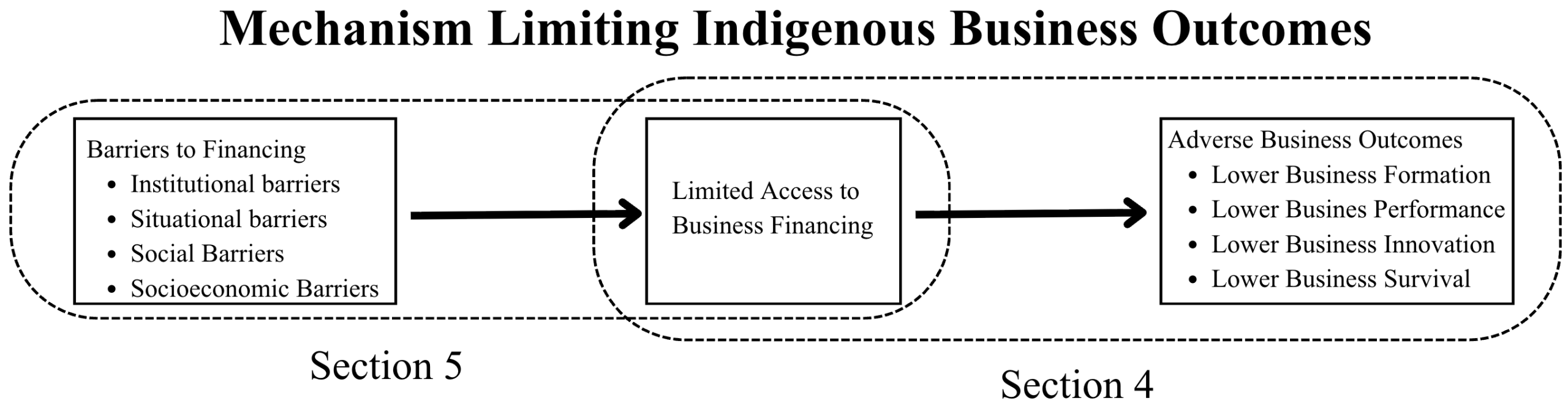

First, this review constructed two theoretical frameworks to guide this paper. Figure 1 presents the first theoretical framework, distinguishing contextual from analytical components. This paper analyzes exclusively the relationship between limited financing access and business outcomes in Section 4. The upstream barriers-to-access pathway serves contextual purposes only in Section 5, with these pathways not being interconnected. The barriers pathway provides necessary context for why financing constraints exist, while the access-to-outcomes pathway constitutes the main analytical focus of this study—examining how financing limitations, once present, affect business outcomes. This clear demarcation ensures the study remains concentrated on financing access as the association of interest rather than conflating it with other mechanisms that might affect business outcomes. The second theoretical framework emerged through an inductive process from a preliminary literature review. Specifically, the four barrier categories emerged from the initial examination of five studies Chernoff & Chueng8, Peredo et al.9, Henriques et al.10, Cooper3, Newman11. Through this preliminary analysis, barriers consistently clustered into four distinct types based on their underlying mechanisms: institutional barriers (constraints associated with formal laws, regulatory frameworks, and administrative procedures), situational barriers (constraints associated with contextual circumstances of place, infrastructure, or environment), social barriers (constraints associated with culture or society), and socioeconomic barriers (constraints associated with unequal social and economic conditions).

Second, the preliminary synthesis was a two-step process of data extraction and thematic categorization. The first step was the extraction of data from each eligible study into Microsoft Excel. Specifically, bibliographic data, methodological characteristics, geographic distinctions, and whether the general focus of the study was on the barrier to limited access to business debt financing or business outcomes were captured into this spreadsheet.

In the second step, following each study’s classification into either barriers to financing or business outcomes, the data underwent thematic categorization conducted by one person using Microsoft Excel. Coding then proceeded using a priori categories as follows: barriers to financing studies were categorized by barrier categories—institutional, situational, social, and/or socioeconomic—while business outcome studies were categorized by business metrics—formation, performance, survival, and/or productivity. Non-mutually exclusive coding was allowed.

Following thematic categorization of both the barrier and business outcome study, all mechanisms and quantitative indicators were extracted for each barrier type or each business metric each study addressed. For instance, if a study classified under business survival identified a mechanism associating limited financing with reduced liquidity and lower survival probabilities, that mechanism was isolated and entered into the spreadsheet. Quantitative measures, such as the finding that Indigenous firms exhibit an 18.41 percent higher exit probability, were likewise recorded. Similarly, if a study categorized under institutional barriers identified a mechanism such as Section 89 of the Indian Act preventing Indigenous entrepreneurs from pledging on-reserve assets as collateral, that mechanism was extracted and recorded in the spreadsheet. Studies addressing multiple barriers and outcomes were coded into all relevant categories.

In addition, as a sole researcher, inter-rater reliability testing was not possible. To enhance coding quality, an iterative two-pass approach was employed. The first pass established initial categorization of all included studies. Following a one-week interval, a second pass systematically refined barrier classifications, verified that extracted mechanisms aligned with operational definitions, and resolved any ambiguities. This iterative refinement process ensured consistent application of the four-barrier framework across all studies. The absence of multiple independent coders represents a methodological limitation; however, the use of an explicit a priori framework with operational definitions and iterative coding provides appropriate rigour for narrative synthesis conducted by an individual researcher.

Third, an analysis of the collected data was conducted to identify recurring patterns and concepts across the different studies. The recurring data were then synthesized into a two-phase narrative to answer the research question. The first phase’s analysis details the specific mechanisms through which business financing exclusion is associated with adverse business outcomes. This meant aggregating the data extracted from the literature within the business outcomes section of the thematic categorization and creating a narrative that saw multiple pathways identified between limited access to business debt financing and the four business outcomes of formation, performance, survival, and productivity. The second phase’s analysis is about the relationship between barriers and limited access to business debt financing within the literature. This was accomplished by analyzing the extracted data to identify, for each of the four barrier categories, the documented pathways through which it is associated with limited access to debt business financing. The narrative for this phase was built by aggregating data extracted from the literature within the barriers to access section of the thematic categorization to create a narrative, showing, for example, how the inability to fulfill collateral requirements due to the Indian Act is associated with reduced ability to access business loans.

Fourth, the methodological rigour of journal articles was established by their peer-reviewed status. For grey literature, trustworthiness was evaluated based on the authority and recognition of the publishing body. Accordingly, only reports from recognized Indigenous-led institutions, governmental departments, or other recognized public bodies were included.

Business Outcomes Disparities between Indigenous and non-Indigenous Businesses

This section examines how Indigenous-owned businesses consistently experience weaker business outcomes across four key dimensions: survival, revenue, productivity, and formation. Notably, these gaps persist even after controlling for confounding factors such as region, industry, rurality, firm age, and firm characteristics.

Business Survival

Indigenous-owned businesses have a lower survival probability than their non-Indigenous counterparts, and this difference persists even after controlling for confounding variables. Analysis by Statistics Canada found—utilizing a Cox proportional hazard model and controlling for business age, business size, capital amount, rurality, province, and industry—Indigenous-owned businesses were 18.41% more likely to exit than their non-Indigenous counterparts12. In addition, by 2018, only 62% of the 2005 cohort of Indigenous-owned businesses survived, two percentage points below the survival rate of non-Indigenous-owned businesses12. This survival disadvantage is associated with liquidity constraints. In 2023, two-thirds (66.3%) of Indigenous majority-owned businesses stated they had enough cash or liquid assets to cover the cost of operations for the next three months, compared to more than three-quarters (76.1%) of all private-sector businesses13. In addition, Indigenous-owned businesses were almost twice as likely as non-Indigenous businesses to not have enough liquidity to cover three months of operations (10.0% vs 5.1%)13. These findings indicate that factors uniquely affecting Indigenous businesses are associated with higher exit rates beyond general economic conditions affecting the wider population.

Business Performance

Indigenous businesses exhibit lower performance even after controlling for observable business characteristics. A Statistics Canada study reveals that after controlling for business age, business size, capital amount, rurality, province, and industry, Indigenous-owned businesses earn 2.7% less in revenue than their non-Indigenous counterparts12. Additional analysis by the Bank of Canada found that Indigenous census subdivisions (CSDs) have lower revenues and profits per resident than non-Indigenous CSDs with the same number of people8. The persistence of revenue disparities across multiple analytical approaches—a firm-level econometric analysis using a multiple regression model to conduct extensive controls and a community-level comparative analysis—demonstrates that Indigenous businesses experience constraints on their ability to generate sales and profits, where these adverse business outcomes cannot solely be attributed to observable business or geographic characteristics.

Business Productivity

Indigenous businesses demonstrate lower productivity levels compared to non-Indigenous businesses, even after controlling for confounding variables. A Statistics Canada study reveals that after controlling for business age, business size, capital amount, rurality, province, and industry, Indigenous-owned businesses are 7.5% less productive than non-Indigenous-owned businesses12. The fact that this productivity gap persists even after controlling confounding variables indicates that factors uniquely associated with Indigenous business ownership contribute to reduced productivity levels. One factor that may explain this difference is the disparities in the amounts of innovation among Indigenous versus non-Indigenous-owned businesses. Analysis by Innovation, Science and Economic Development (ISED) Canada using the 2020 Survey on Financing and Growth of SMEs found Indigenous-owned businesses demonstrated significantly lower innovation rates than all other demographic groups14. Indigenous SMEs saw an innovation propensity of 21.6, compared to 28.4 of all Canadian SMEs, with all other measured demographic categories performing significantly better than Indigenous SMEs14. And only 11.5% of Indigenous SMEs introduced a new or significantly improved product versus 16.4% nationally, with Indigenous businesses again ranking lowest by a 4% margin among all demographic groups measured14. However, since this ISED Canada study does not control for other socio-demographic factors, this difference may also be driven by other underlying differences such as educational background or location. In all, the persistence of productivity gaps across extensive controls suggests Indigenous businesses face unique challenges for increased productivity not faced by the general population of Canadian businesses, though whether lower innovation rates mediate this productivity gap requires further investigation with appropriate controls.

Business Formation

Indigenous entrepreneurs in Canada see lower rates of business formation compared to their non-Indigenous counterparts. As seen in Figure 28, while business formation rates between Indigenous and non-Indigenous businesses were comparable and occasionally favoured Indigenous businesses between 2006 and 2013, a recent and ever-widening gap has emerged since 2013, with Indigenous business formation rates declining relative to non-Indigenous rates. In addition, analysis by the Bank of Canada found that in 2018 only 39 out of every 1,000 Indigenous people aged 15 to 64 own a business, compared to 108 out of every 1,000 non-Indigenous people in the same age group8. Furthermore, by the end of 2022, there were 17,417 private businesses in Canada owned by Indigenous people. This is only 1.7% of all 1,011,474 private sector businesses, even though Indigenous people make up 5% of Canada’s population13. The current underrepresentation and recent divergence in formation trends indicate that barriers are preventing Indigenous entrepreneurship from keeping pace with the broader Canadian economy. However, it remains unclear from existing studies whether this divergence in formation rates stems from factors uniquely associated with Indigenous entrepreneurs or from broader structural and market conditions and thus requires further investigation with appropriate controls.

Phase 1: Business Financing as a Potential Mechanism

This section proposes limited access to business financing as a potential mechanism explaining the business outcome disparities documented in Section 3, first establishing why financing is relevant for business outcomes generally, then documenting the substantial financing gaps faced by Indigenous businesses specifically. Although other mechanisms that are associated with disparities in Indigenous business outcomes certainly exist within the literature, the findings presented below synthesize only those associated with financing constraints.

Financing and Business Outcomes

Business financing serves as a foundational input across the entire business lifecycle. The literature documents associations between limited access to financing and every stage of business development—from maintaining liquidity to improving productivity and performance and business formation. First, when businesses face economic recessions, revenue declines, or unexpected expenses, they require immediate access to credit lines or emergency funds to cover liquidity gaps15. On the other hand, the absence of this safety net means businesses cannot cover operational costs during temporary downturns, which is linked to creating a premature shutdown of the affected businesses15‘16. Second, businesses require capital to create the infrastructure needed to realize new revenue opportunities. However, as best articulated by an on-reserve Indigenous entrepreneur interviewed by the CCIB and GAC: “I find it difficult to receive financing to help build my business. With no financing for the business, I’m struggling to be able to hire any employees so that I can produce larger orders and generate more revenue”17. This Indigenous entrepreneur’s statement captures how limited access to financing is associated with reduced investments in expansion levers such as increased staff, equipment, and inventory, which correlates with lower revenue and profit generation capability. Third, productivity improvements depend on capital for technology adoption, equipment upgrades, employee training programs, and research and development activities to create innovation within a business4. Without access to financing for these productivity-enhancing investments, Indigenous businesses are associated with being constrained to suboptimal processes that yield lower output per worker or are unable to fund research and development activities to create better products4. The former Deputy Governor of the Bank of Canada, Lawrence Schembri4, noted this association, stating that restricted capital access is linked to “the productivity of Indigenous businesses and workers.” Fourth, capital is central to new business, as new businesses require upfront capital investments in equipment, inventory, commercial premises, and working capital to begin operations3. The literature indicates that entrepreneurs unable to secure startup financing face barriers to acquiring the necessary assets for business launch, which is associated with lower business entry rates regardless of entrepreneurial ability or market opportunity3‘18. The pattern of undercapitalization among Indigenous entrepreneurs coincides with the recent and widening business formation gap noted above, wherein Indigenous entrepreneurs create businesses at rates far below their population share in contexts characterized by limited access to business financing8.

Evidence of Indigenous Financing Gaps

Indigenous businesses face substantially lower access to business financing compared to non-Indigenous businesses across multiple quantitative measures. Export Development Canada19 reports that while Canadian businesses achieve a 90% loan approval rate, approval rates for Indigenous businesses drop dramatically to 58%. Additionally, Indigenous entrepreneurs’ access to capital is minimal. This is seen in a study by the Bank of Canada showing that in 2013, Indigenous businesses accessed only 0.2% of the total available capital in Canada and received just $9 for every $100 in market-sourced financing accessed by non-Indigenous businesses8. The convergence of findings from Export Development Canada19 and the Bank of Canada8 establishes a clear pattern of exclusion, where Indigenous businesses face both significantly lower loan approval rates and severely restricted access to the total capital pool. In total, the House of Commons Standing Committee on Indigenous and Northern Affairs reports a $175 billion capital gap within the Indigenous economy20.

However, this disparity in access to business debt financing cannot solely be explained by factors affecting the general Canadian population, such as geography. Instead, this disparity can be more suitably explained by Indigenous-specific factors that uniquely affect Indigenous entrepreneurs or businesses. Recent literature includes studies that, through statistical means, control for remoteness or type of industry, among other variables, which can isolate the independent effect of being an Indigenous entrepreneur or firm on business financing. The first such study is an econometric study by the Canadian Council for Indigenous Business & Global Affairs Canada17. This study conducted a survey of over 2600 Indigenous SMEs—named the Survey of Indigenous Firms—and utilized Statistics Canada’s Survey of Financing and Growth of SMEs, and, after controlling for remoteness, virtual-sales capacity, industry sector, and firm size, the study found Indigenous SMEs are 1.3 times more likely to report financing as a growth barrier than non-Indigenous SMEs17. These results demonstrate that financing gaps persist independently of geography, sector, or business structure, indicating that limited access to capital arises not solely from rurality or industry composition but from Indigenous-specific exclusionary mechanisms in Canada’s financing system.

Another study from the Bank of Canada, using the Survey of Indigenous firms and the Bank of Canada’s Business outlook survey, found Indigenous firms were 3.8 times less likely to rely on bank financing than non-Indigenous firms, though this specific comparison is descriptive and does not include statistical controls. In addition, this study found, from the Survey of Indigenous Firms, that 51% of these Indigenous-owned businesses were located within Indigenous communities, of which about 70% were in rural areas21. However, even after controlling for firm size, incorporation, revenue, profitability, Indigenous identity, and industry sector, the study found that the independent effect of being rural on Indigenous-owned businesses’ ability to access finance was statistically insignificant21. The conclusion that can be drawn from such a result is that geographic remoteness alone does not explain Indigenous firms’ lower access to financing21. Instead, the persistence of financing barriers after controlling for location and firm characteristics suggests that Indigenous-specific factors, rather than spatial isolation, are the primary drivers of limited business financing among Indigenous-owned businesses.

An international study from Bolivia utilized a controlled laboratory–field experiment that used fictitious but financially identical small business loan applications that differed only by ethnic identity, allowing the authors to isolate the independent effect of Indigeneity on loan approval22. Credit officers were asked to evaluate each application under real lending conditions. Using a Bayesian mixed-effects logistic regression model, the study found that Indigenous identity alone significantly reduced loan approval outcomes even after controlling for all financial and demographic characteristics22. This demonstrates that indigeneity itself—not income, collateral, or geography—can shape financing decisions. Thus, the study provides experimental evidence that Indigenous people operate independently from conventional credit-risk factors when it comes to their ability to obtain business debt financing.

Another international study was conducted by the Federal Reserve Bank of Cleveland. This study utilized the Federal Reserve’s Small Business Credit Survey from 2016 to 2020 and found, after controlling for business size, business age, revenue, profitability, industry, and geography, that Native American-owned businesses received significantly higher credit denial rates from conventional financial institutions compared to similar white-owned businesses23. Furthermore, when examining the Paycheck Protection Program (PPP), the study further revealed that, even after accounting for business size, business age, revenue, profitability, industry, geography, and both owner and business credit scores, Native American businesses were significantly more likely to receive only partial the originally requested funding amount and were significantly more likely to be discouraged from applying for PPP loans compared to similar white-owned businesses23. Notably, the disparities between Native American-owned businesses and white-owned businesses for credit denial and amount were greater than those between other ethnic minorities, such as Black, Asian, and Hispanic-owned business23.

Phase 2: Mechanisms Creating Limited Access to Business Financing

This section identifies the specific barriers that constrain Indigenous entrepreneurs’ access to business financing. Drawing on qualitative and quantitative evidence, it documents four categories of barriers—institutional, situational, social, and socioeconomic—that interact to create the financing gaps documented in section 4.

Institutional Barriers

Institutional barriers represent a significant obstacle restricting on-reserve Indigenous entrepreneurs’ access to business financing. The Indian Act prevents property on reserve from being seized as collateral under Section 894‘18‘24. This provision emerged from the late 19th-century colonial framework that sought to “protect” Indigenous lands from sale or seizure while simultaneously restricting Indigenous peoples’ economic autonomy24‘18. Specifically, during this period, predatory lending practices and fraudulent land transactions frequently resulted in Indigenous land loss. Section 89 was designed to prevent such seizures by making on-reserve property legally inalienable11. While intended as protection, this provision effectively prevents on-reserve Indigenous entrepreneurs from using their property as collateral11. This provision is important because collateral is necessary for obtaining commercial loans, as it provides an asset that can be recovered if the borrower defaults on the loan9‘18‘4. In other words, collateral acts as a safeguard for lenders. Thus, the absence of collateral significantly reduces on-reserve Indigenous people’s ability to obtain business financing9‘18.

In addition to the inability to pledge collateral, the Indian Act contains many regulatory gaps not present in off-reserve settings that may suppress on-reserve Indigenous entrepreneurs’ access to financing16. These regulatory gaps, which include the absence of enforceable property rights, incomplete contractual frameworks, and the lack of a reliable land title registry, create regulatory uncertainty for business activity16. Moreover, excessive bureaucratic processes increase transaction costs and timelines from Indigenous-related governmental departments18‘20. As well, Indigenous nations’ unique legal status as self-governing entities adds another layer of regulatory uncertainty, as disputes often arise over whether federal, provincial, or Indigenous law governs financial arrangements11.

The cumulative effect of these institutional barriers is that the cost of doing business on reserves is often four to six times higher than the cost off reserves, with transactions taking up to five times longer to process8‘16‘18. Lenders, who prefer predictable regulatory environments and more friendly business environments, may respond by rationing business financing to on-reserve Indigenous entrepreneurs, which may be linked to their limited access to business financing8‘11‘18.

Situational Barriers

Situational barriers are the most immediate barrier for many on-reserve Indigenous entrepreneurs when accessing business debt financing. The geographic isolation of reserves seen today is no natural condition but the product of a colonial policy of systemic forced land dispossession enacted by the Government of Canada in the 19th century8. This policy forcibly relocated Indigenous peoples from territories with abundant natural resources or close proximity to metropolitan regions to lands with limited economic value and substantial distance from population centres8. According to the Bank of Canada, approximately seventy percent of Indigenous reserves are located more than fifty kilometres from the nearest service centre8. As well, the median distance from an Indigenous band council to the closest bank branch is 23.9 km, compared to only 1.3 km between a rural non-Indigenous census subdivision in 201925‘26.

This distance to financial institutions may limit the multistage processes required for commercial loan applications, which often demand a litany of in-person activities such as multiple in-person meetings, document verification and exchange, and building trust and a working relationship with the lender27. Added to that is poor transportation infrastructure, which may exacerbate the problem because some reserves are accessible only by dirt or seasonal roads25. Factors such as distance and accessibility issues make bank visits for commercial loan applications not only costly but also time-consuming.

The availability of bank branches is also limited. Fewer than 50 bank outlets operate across nearly 3,400 reserves nationwide28‘1. At the same time, branch numbers across Canada and within Indigenous reserves fell from 8,895 in the fourth quarter of 2019 to 8,436 in the fourth quarter of 202226. This trend reflects the bank’s assumption that most customers prefer the convenience of online lending and banking. For Indigenous reserves, however, this shift is associated with lower levels of access to business debt financing. The literature reveals a pattern of what Sutton-Lalani et al.29 describe as “double marginalization,” where some Indigenous reserves are disadvantaged on two intersecting points of access. First, large geographic distance, accessibility issues, and the declining number of bank branches limit physical access to commercial loan services. Second, many reserves are unable to rely on digital loan-application systems or online financing portals. Specifically, more than a quarter of Indigenous households (25.5%) may be unable to effectively utilize online credit portals because of internet speeds of less than 10 Mbps in 2019. By contrast, almost 13% of all rural Canadian households saw internet speeds less than 10 Mbps in 2019, reflecting the digital divide between Indigenous on-reserve households and the rest of Canada25.

Double marginalization may severely hamper the ability for affected Indigenous reserves to access business debt financing. Long distances and declining bank branches make conducting in-person loan consultations unfeasible or impractical, while poor internet access prevents digital loan submissions from supplementing for the lack of physical access25‘29. In sum, weak physical banking infrastructure, accessibility issues, and poor digital connectivity combine to make the process of obtaining business debt financing logistically burdensome and, for some Indigenous entrepreneurs, effectively inaccessible, all of which is linked to Indigenous people’s lower access to business debt financing.

Social Barriers

Cultural differences between Western and Indigenous approaches to entrepreneurship are associated with social barriers that limit Indigenous entrepreneurs’ access to financing. Mainstream entrepreneurship is generally defined by individualism and profit-seeking, where the creation and management of ventures by individuals is for the purpose of seeking profit maximization and individual wealth accumulation9. In contrast, “Indigenous entrepreneurship is seen as aimed not at individual economic benefit but at multiple goals… such as self-determination and heritage preservation, but also immediate benefits such as medical and elder care”9. In addition, Indigenous entrepreneurs embed in their ventures Indigenous values of reciprocity, environmentalism, and community well-being. As such, entrepreneurship is more so a tool to solve their communities’ socioeconomic issues rather than merely accumulating individual wealth9. Thus, Indigenous entrepreneurs pursue blended goals that combine economic returns with social, cultural, and environmental objectives9‘10.

However, the Indigenous approach to business may conflict with how mainstream financial institutions evaluate businesses. Conventional lenders utilize profit-based frameworks such as projected profitability or ROI to evaluate the success of a venture. This framework cannot quantify non-financial outcomes such as environmental protection, which mainstream lenders might interpret as lacking profit potential9. The literature, therefore, suggests that this inability to translate blended goals into profit-only metrics is associated with Indigenous entrepreneurs’ ventures being undercapitalized9‘10.

The case of the Hupacasath First Nation provides an example of this pattern. The nation was trying to build a hydroelectric dam in their traditional territory that abided by their values of environmental stewardship and community benefit while still generating economic returns10. However, when seeking financing needed for the venture, the Hupacasath encountered the same dynamic described above. The Hupacasath approached Canada’s most important financial institutions, but all rejected their funding applications, as they were unable to assess the project’s positive impact on the environment or the benefits to the community alongside economic returns10. Only Vancity Credit Union—Canada’s largest credit union, which evaluated the ventures’ social, environmental, and economic returns simultaneously—agreed to finance this venture10. This case highlights how Canada’s banks’ inability “in assessing the social and environmental benefits/costs of projects”10 may restrict Indigenous entrepreneurs to financial institutions that share their broader value10. Thus, the Hupacasath case shows how mainstream banks’ narrow focus on financial returns is associated with excluding Indigenous entrepreneurs’ ventures from business debt financing10.

Socioeconomic barriers

Socioeconomic barriers add an additional obstacle for some Indigenous entrepreneurs. The beginnings of Indigenous lower socioeconomic status can be found in Canada’s various colonial policies. The reserve system constituted the first such policy. Indigenous peoples’ traditional means of economic self-sufficiency—farming, hunting, and fishing—were systematically uprooted as they were displaced from their traditional territories and confined to reserves with inadequate resources to support their customary livelihoods30‘31. This, along with discriminatory legislation that outlawed resource distribution and severely limited Indigenous peoples’ ability to fish and hunt, led to rapid increases in poverty on reserves31. The second such piece of policy was the pass system, which lasted from 1885 to 1941. This system confined Indigenous peoples to reserves and limited their ability to leave, seek employment, or participate in broader economic activities. This restriction undermined traditional economies and entrepreneurship, eroding self-sufficiency and increasing poverty32‘33. The third such policy is the residential school system, lasting from the 1870s to 1996 and was a system of schools jointly administered by the Government of Canada and the Catholic Church34‘35. Such schools forcibly removed approximately 150,000 Indigenous children from their families with the explicit goal of cultural assimilation34‘35. These facilities prioritized revenue-generating activities such as domestic work or farming over educational instruction, where it was common for children to attend schools for a decade yet receive nothing more than a Grade two education35. These facilities were underfunded, overcrowded, poorly heated, had inadequate sanitation, and lacked proper medical care, creating conditions where abuse, malnutrition, disease, and death were common34‘35. The effects of such institutions are strongly linked to lower educational attainment and reduced employment opportunities. Relative to Indigenous children whose parents did not attend residential schools, Children of survivors are 6.5-8.4 percentage points less likely to graduate, have 3-6% reduced level of attendance from high school, are significantly more likely to be suspended or expelled, and are 3% less likely to be employed even after holding confounding variables such as gender, First Nation/Métis/Inuit identity, Status Indian registration, CSD, and year of birth constant34‘35.

The first component of socioeconomic barriers is educational disadvantage. Numeracy and literacy skills are pertinent to filling in loan applications, writing business plans, and pitching related activities24‘18. However, the 2012 Programme for the International Assessment of Adult Competencies showed that Indigenous adults performed lower in literacy and numeracy than non-Indigenous adults36.

In addition to numeracy and literacy skills, financial literacy is equally important to accessing finance. Entrepreneurs with greater financial literacy can more effectively maintain the financial documentation required by lenders to make lending decisions and promote better financial management for their businesses, which also creates higher credit ratings37. In other words, strong financial literacy is associated with an improved likelihood of loan approval. On the flip side, entrepreneurs with limited financial literacy may not have prepared all the required financial documentation, which is associated with automatic loan rejection37. They also may appear to have higher risks that result from their limited ability to understand loan terms and manage debt and the business’s finances, which also drags down the business’s credit rating37.

Indigenous entrepreneurs face a significant disadvantage in terms of financial literacy. While rural-specific comparison data would provide a more appropriate baseline, such disaggregated data are not publicly available from national surveys, and national-level benchmarks represent the best available evidence for establishing baseline understanding of the financial literacy disparities. According to the 2024 Canadian Financial Capability Survey (CFCS), 69% of Indigenous people had difficulty keeping up with bills and financial commitments, compared to 60% of Canadians overall38. Additionally, 65% of Indigenous people relied on credit to pay for daily expenses, compared to 48% of Canadians overall38. Furthermore, 35% of Indigenous people currently have a Registered Retirement Savings Plan, compared to 47% of Canadians overall38. In sum, the data from the 2024 CFCS shows that Indigenous financial literacy challenges exceed those of the general Canadian population, where the dataset of the latter includes the rural population of Canada.

In addition to educational disadvantages, Indigenous people also experience significant income and employment disparities. In 2020, the unemployment rate among Indigenous people was 11.6%, compared with 7.8% across all rural areas39‘40. Indigenous people also had a household median after-tax income of $71,500, compared with $72,500 across all rural areas41‘42.

These various socioeconomic disadvantages are associated with barriers to accessing business financing. This is because lenders assess eligibility for business financing through creditworthiness benchmarks, and these benchmarks consist of maintaining prime credit scores, consistent repayment histories, and low credit utilization rates27. However, lower incomes and unemployment may impede Indigenous entrepreneurs from meeting these benchmarks18‘1. In particular, lower incomes and unemployment may increase the likelihood of missed debt obligations and higher credit utilization, both of which heavily weaken credit scores43. These lower socioeconomic outcomes correlate with lower credit scores for Indigenous entrepreneurs than non-Indigenous entrepreneurs. As it stands, there is currently no nationwide data on Indigenous and non-Indigenous entrepreneurs’ credit scores. The only available evidence is from NACCA & BDC18, which reported that the average credit scores in six Indigenous reserves in 2015 were 657, roughly 100 points lower than Ottawa’s households’ average of 761 in the same year. Although this data lacks generalizability to Indigenous people nationally, it provides a “first cut” of Indigenous entrepreneurs’ difficulty meeting traditional creditworthiness criteria and speaks to the need for comprehensive data collection regimes that include greater Indigenous data.

Barrier Interaction

The four barrier categories do not operate independently. Instead, they interact to create compounding effects. This section will document the interactions that occur between the four categories of barrier within the literature. It should be noted that the list of interactions presented here is not an exhaustive account of every possible combination. Instead, it represents a record of the interactions that are explicitly documented in the scholarly literature.

The first barrier interaction for business debt financing, described by Peredo et al.9 and Henriques et al.10, sees institutional and social barriers intersect in ways associated with reduced Indigenous entrepreneurs’ access to business debt financing. Business lending typically follows a standard pathway of entrepreneurs pledging collateral and lenders assessing business viability3. Section 89 of the Indian Act blocks the first element, forcing reliance entirely on business model assessment10‘9. However, Indigenous business models are unconventional in that they pursue profit equally with other priorities, such as environmental and social goals. The literature indicates that the unconventionality of Indigenous business models is associated with mainstream banks viewing the businesses as unprofitable and rejecting credit requests from Indigenous entrepreneurs10‘9.

The second barrier interaction for business debt financing, described by the First Nations Financial Management Board15, combines social and socioeconomic barriers. Business lending typically relies on standardized credit assessments that evaluate borrowers based on stable income, consistent employment history, and established creditworthiness27. However, Indigenous entrepreneurs experience significantly lower median incomes, higher unemployment rates, and persistent wealth gaps41‘39‘1. These socioeconomic realities mean Indigenous borrowers are less likely to meet conventional creditworthiness benchmarks. Financial institutions may further compound this disadvantage through interpreting Indigenous business models as unprofitable due to their business models pursuing profit equally with other priorities, such as environmental and social goals9‘10.

The third barrier interaction for business debt financing, as articulated by Kremer & Mah44, combines situational and socioeconomic factors. Many Indigenous reserves are situated far from financial institutions25. This spatial isolation imposes direct costs that make it costly and time-consuming for entrepreneurs to access lenders, submit applications, or maintain relationships with banks44. Thus, this creates situations where Indigenous entrepreneurs who have fewer resources may struggle to afford repeated travel44. Consequently, the situational barrier of distance is associated with compounded social and socioeconomic inequities, which correlates with restricted opportunities to secure financing44.

Contextual Dominance

The four barriers do not just compound; some barriers operate with dominance over others in certain circumstances. This section explores how institutional and situational barriers operate with dominance in on-reserve settings, but, in off-reserve settings, socioeconomic and social barriers become the dominant barriers associated with restrictions on access to business debt financing for Indigenous-owned businesses.

In an on-reserve context, institutional barriers operate with the most dominance. At the outset, due to the inability to pledge collateral, on-reserve Indigenous entrepreneurs are structurally prohibited at the legal or regulatory level from accessing business debt financing4. In other words, an on-reserve entrepreneur may have a viable business plan, strong financial literacy, and cultural alignment with Western business models, but the legal infrastructure precludes the loan from being structured in the first place. Beyond collateral restrictions, regulatory gaps created by the Indian Act—absent enforceable property rights, incomplete contractual frameworks, and lack of reliable land title registries—create regulatory uncertainty that manifests in transaction costs four to six times higher than off-reserve contexts with processing timelines five times longer, which is associated with prompting lenders to engage in credit rationing to on-reserve entrepreneurs16.

After institutional barriers, situational barriers are the second most dominant barrier to operate within on-reserve settings that constrain Indigenous entrepreneurs’ business debt financing. In this domain, many on-reserve indigenous entrepreneurs, through the double marginalization articulated in previous section 5.2, are not only unable to access financing through physical channels (too distant) but also unable to access digital channels (inadequate connectivity)29‘25. Critically, social and socioeconomic barriers become functionally irrelevant in on-reserve contexts because institutional and situational barriers effectively prevent entrepreneurs from reaching the evaluation stage where business models or creditworthiness would be assessed. In other words, it is not pertinent whether an entrepreneur’s business pursues blended goals or pure profit maximization or whether they have excellent or poor financial literacy; institutional and situational barriers already impose restrictions to business debt financing in an absolute manner.

Within off-reserve settings, institutional and situational barriers do not apply—off-reserve Indigenous entrepreneurs can pledge collateral without Section 89 restrictions and have geographic proximity to financial institutions with adequate digital infrastructure—meaning Indigenous entrepreneurs can participate in the financing system. However, this shifts the locus of exclusion from structural barriers to evaluative barriers, with socioeconomic barriers achieving primary dominance. In the evaluation stage, socioeconomic status—credit scores, financial literacy, income, and employment—becomes strongly associated with application outcomes27. Standardized credit assessments evaluate applicants through credit histories, debt-to-income ratios, and employment status, and Indigenous people systematically underperform on these metrics, which may be associated with their rejections from business debt financing39‘41.

Social barriers operate as the secondary constraint in off-reserve contexts. These barriers relate to the cultural mismatch between Indigenous and Western business models, which may compound this socioeconomic exclusion by adding an additional layer of evaluative rejection, but they operate as a secondary constraint—the primary mechanism of off-reserve exclusion appears to be socioeconomic barriers associated with entrepreneurs failing creditworthiness screening9‘10.

Limitations

This literature review faces several methodological and empirical constraints that impact the generalizability of its findings. The narrative synthesis approach inherently limits the ability to establish causal relationships. In addition, throughout this review, correlational evidence has been used to identify associations linking limited access to business debt financing to business outcomes or financing barriers to limited access to business debt financing. The cross-sectional nature of most included studies limits the ability to isolate the independent effects of limited access to business debt financing from other socioeconomic disadvantages that Indigenous entrepreneurs and businesses experience. In sum, while patterns suggest relationships between limited business financing access and adverse business outcomes, readers should interpret these connections as correlations rather than definitive causal relationships.

In addition, the available literature on Indigenous business financing in Canada remains limited in both breadth and granularity, which constrains generalizability. These gaps necessitate reliance on a small number of recent studies that, while methodologically sound, do not yet provide full coverage across all regions and business segments. However, this still represents the best available evidence and underscores the persistent gaps in Indigenous business and financing data collection. More detailed information on research gaps will be found in the following section.

Research Agenda

The evidence limitations and methodological constraints identified in this review reveal two critical research priorities that would advance understanding of Indigenous business financing barriers and inform more effective policy interventions.

Comprehensive Data Collection

Current literature is mostly cross-sectional studies that establish correlational rather than causal relationships between business financing barriers and business outcomes8‘38. Future research should prioritize multi-year longitudinal designs tracking the same Indigenous individuals and businesses to establish definitive causation. Such studies would provide more insights and evidence necessary for targeted policies while controlling for confounding socioeconomic barriers that currently obscure the independent effects of limited business financing access. In addition, this review also reveals systematic gaps in Indigenous financial data collection. A starting point could be creating comprehensive national measurements of loan approval rates, credit score comparisons, and business financing volumes. Additionally, other data gaps that are in need of further data collection are Indigenous business capital expenditures and export participation8. Without such foundational data, policymakers would lack comprehensive information, potentially leading to ineffective interventions that fail to comprehensively address barriers to Indigenous business debt financing.

Policy Intervention Evaluation

While existing literature effectively documents barriers to Indigenous business financing, research on the effectiveness of potential solutions remains limited. Although some evaluation literature exists, such as for Aboriginal Financial Institutions and government lending programs, broader policy intervention research on expanding Indigenous entrepreneurs’ access to commercial lending and investment capital is scarce. Some starting points for policy intervention research include mobile business lending programs that bring credit officers directly to remote communities or creating mainstream loan guarantees and collateral-support mechanisms. More intervention research would provide evidence-based guidance for scaling successful approaches while avoiding ineffective policies that fail to address the barriers to financing.

Conclusion

This review demonstrates that Indigenous entrepreneurs in Canada experience lower business formation, performance, productivity, and survival and lower access to business financing—even after accounting for confounding variables such as poverty and rurality. The paper addresses its two research objectives through a two-phase synthesis. First, it identified four pathways through which limited access to business financing is associated with adverse outcomes for Indigenous-owned businesses, specifically the business formation, performance, innovation, and survival pathways. Second, it outlines the institutional, situational, social, and socioeconomic barriers that are associated with Indigenous entrepreneurs’ reduced access to financing Yet, given the cross-sectional nature and limitations of available data, these conclusions should be viewed as a “first cut” into the relationship between restricted debt financing and Indigenous business outcomes, with the proposed mechanism representing a potential mechanism rather than an empirically established causal relationship operating in real-world conditions. In organizing the literature, this research shows that barriers to business debt financing are linked to suppressed entrepreneurship and weaker business performance outcomes, which highlights the importance of equitable access to business debt financing. In conclusion, given that business debt financing is associated with beneficial business outcomes, the Government of Canada must implement concrete policies that close the persistent gaps in business financing in a rapid manner, with particular attention to addressing the institutional, situational, social, and socioeconomic barriers.

References

- Indigenous Services Canada. An update on the socio-economic gaps between Indigenous peoples and the non-Indigenous population in Canada: highlights from the 2021 census. 2023. https://www.sac-isc.gc.ca/eng/1690909773300/1690909797208. [↩] [↩] [↩] [↩]

- C. P. Lakuma, R. Marty, F. Muhumuza. Financial inclusion and micro, small, and medium enterprises (MSMEs) growth in Uganda. Journal of Innovation and Entrepreneurship. Vol. 8, pg. 15, 2019, https://doi.org/10.1186/s13731-019-0110-2. [↩]

- T. Cooper. Indigenous business in Canada: principles and practices. Cape Breton University Press, 2016. [↩] [↩] [↩] [↩] [↩] [↩]

- L. L. Schembri. The next generation: innovating to improve Indigenous access to finance. Fraser Institute, 2023. [↩] [↩] [↩] [↩] [↩] [↩] [↩]

- Government of Canada. Indigenous peoples and human rights. 2024. https://www.canada.ca/en/canadian-heritage/services/rights-indigenous-peoples.html. [↩]

- J. N. Ssentamu. Debt financing by commercial banks and the profitability of small and medium size enterprises (SMEs) in Kampala. Uganda Technology and Management University, 2015. [↩]

- J. Popay, H. Roberts, A. Sowden, M. Petticrew, L. Arai, M. Rodgers, N. Britten, K. Roen, S. Duffy. Guidance on the conduct of narrative synthesis in systematic reviews: a product from the ESRC methods programme. Lancaster University, 2006, https://doi.org/10.13140/2.1.1018.4643. [↩]

- A. Chernoff, C. Cheung. An overview of the Indigenous economy in Canada. 2023, https://doi.org/10.34989/SDP-2023-25. [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩]

- A. M. Peredo, B. Schneider, A. M. Popa. Indigenous entrepreneurial finance: mapping the landscape with Canadian evidence. In D. Lingelbach (Ed.), De Gruyter handbook of entrepreneurial finance, pg. 335–358, De Gruyter, 2022, https://doi.org/10.1515/9783110726312-022. [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩]

- I. Henriques, R. Colbourne, A. M. Peredo, R. B. Anderson. Relational and social aspects of Indigenous entrepreneurship. In Indigenous wellbeing and enterprise (1st ed.), pg. 313–340, Routledge, 2020, https://doi.org/10.4324/9780429329029-13. [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩]

- D. G. Newman. Public choice and proposed methods of overcoming barriers to Indigenous finance. SSRN Electronic Journal, 2022, https://doi.org/10.2139/ssrn.4163211. [↩] [↩] [↩] [↩] [↩]

- L. Kuate. Survival rate and performance of Indigenous-owned businesses. 2024, https://doi.org/10.25318/11F0019M2024006-ENG. [↩] [↩] [↩] [↩]

- Statistics Canada. Indigenous-owned businesses in Canada: confronting challenges, forecasting growth. 2023, https://www.statcan.gc.ca/o1/en/plus/2762-indigenous-owned-businesses-canada-confronting-challenges-forecasting-growth. [↩] [↩] [↩]

- G. Dewan. SME profile ownership demographics statistics. 2022. https://ised-isde.canada.ca/site/sme-research-statistics/sites/default/files/attachments/2022/h_03166a_en.pdf. [↩] [↩] [↩]

- First Nations Financial Management Board. Addressing gaps in Indigenous access to finance pre-scoping report. 2023. https://fnfmb.com/sites/default/files/2024-01/2023-10-16_idb_pre-scoping_study_final_report.pdf. [↩] [↩] [↩]

- Canadian Association of Native Development Officers, Canadian Council for Aboriginal Business, Indigenous Works, National Aboriginal Capital Corporations Association, National Indigenous Economic Development Board. National Indigenous economic strategy for Canada. 2022. https://niestrategy.ca/wp-content/uploads/2022/05/NIES_English_FullStrategy.pdf. [↩] [↩] [↩] [↩] [↩]

- Canadian Council for Indigenous Business, Global Affairs Canada. Atāmitowin: identifying and overcoming challenges facing Indigenous exporters. 2024. https://international.canada.ca/en/global-affairs/corporate/transparency/reports-publications/chief-economist/inclusive/2024-09-indigenous. [↩] [↩] [↩]

- National Aboriginal Capital Corporations Association, Business Development Bank of Canada. Barriers to Aboriginal entrepreneurship and options to overcome them. 2017. http://nacca.ca/wp-content/uploads/2017/04/Research-Module-3_NACCA-BDC_Feb14_2017.pdf. [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩] [↩]

- Export Development Canada. Building trust with Indigenous businesses. 2023. https://www.edc.ca/en/article/building-relationships-with-indigenous-businesses.html. [↩] [↩]

- House of Commons Standing Committee on Indigenous and Northern Affairs. Barriers to economic development in Indigenous communities. 2022. ourcommons.ca/Content/Committee/441/INAN/Reports/RP11714230/inanrp02/inanrp02-e.pdf. [↩] [↩]

- C. Cheung, J. Fudurich, J. Shah, F. Suvankulov. Survey of Indigenous firms: a snapshot of wages, prices and financing in the Indigenous business sector in Canada. 2024, https://doi.org/10.34989/SDP-2024-4. [↩] [↩] [↩]

- R. Gonzales Martínez, G. Aguilera‐Lizarazu, A. Rojas‐Hosse, P. Aranda Blanco. The interaction effect of gender and ethnicity in loan approval: a Bayesian estimation with data from a laboratory field experiment. Review of Development Economics. Vol. 24, pg. 726–749, 2020, https://doi.org/10.1111/rode.12607. [↩] [↩]

- B. R. Barkley, M. E. Schweitzer. Credit availability for minority business owners in an evolving credit environment: before and during the COVID-19 pandemic. Working Paper (Federal Reserve Bank of Cleveland), 2022, https://doi.org/10.26509/frbc-wp-202218. [↩] [↩] [↩]

- Prosper Canada, AFOA Canada. The shared path: First Nations financial wellness. 2019. https://prospercanada.org/News-Media/News/The-Shared-Path-First-Nations-financial-wellness-r.aspx. [↩] [↩] [↩]

- H. Chen, W. Engert, K. Huynh, D. O’Habib. An exploration of First Nations reserves and access to cash. 2021, https://doi.org/10.34989/SDP-2021-8. [↩] [↩] [↩] [↩] [↩] [↩]

- H. Chen, D. O’Habib, H. Y. Xiao. How far do Canadians need to travel to access cash? 2023, https://doi.org/10.34989/SDP-2023-28. [↩] [↩]

- BMO. How to get a business loan in Canada. 2022. https://www.bmo.com/main/business/news/how-to-get-business-loan/. [↩] [↩] [↩] [↩]

- Indigenous Corporate Training. 11 challenges for Indigenous businesses. 2017. https://www.ictinc.ca/blog/11-challenges-for-indigenous-businesses. [↩]

- A. Sutton-Lalani, S. Hernandez, J. Miedema, J. Dai, B. Omrane. Redefining financial inclusion for a digital age: implications for a central bank digital currency. 2023, https://doi.org/10.34989/SDP-2023-22. [↩] [↩] [↩]

- Government of Canada. Highlights from the report of the royal commission on Aboriginal peoples. 2010. https://www.rcaanc-cirnac.gc.ca/eng/1100100014597/1572547985018. [↩]

- A. Malli, H. Monteith, E. C. Hiscock, E. V. Smith, K. Fairman, T. Galloway, A. Mashford-Pringle. Impacts of colonization on Indigenous food systems in Canada and the United States: a scoping review. BMC Public Health. Vol. 23, pg. 2105, 2023, https://doi.org/10.1186/s12889-023-16997-7. [↩] [↩]

- P. J. Kim. Social determinants of health inequities in Indigenous Canadians through a life course approach to colonialism and the residential school system. Health Equity. Vol. 3, pg. 378–381, 2019, https://doi.org/10.1089/heq.2019.0041. [↩]

- R. Nelson. Beyond dependency: economic development, capacity building, and generational sustainability for Indigenous people in Canada. Sage Open. Vol. 9, pg. 2158244019879137, 2019, https://doi.org/10.1177/2158244019879137. [↩]

- D. L. Feir. The intergenerational effects of residential schools on children’s educational experiences in Ontario and Canada’s western provinces. International Indigenous Policy Journal. Vol. 7, 2016, https://doi.org/10.18584/iipj.2016.7.3.5. [↩] [↩] [↩] [↩]

- M. E. C. Jones. The intergenerational legacy of Indian residential schools. Demography. Vol. 61, pg. 1871–1895, 2024, https://doi.org/10.1215/00703370-11679677. [↩] [↩] [↩] [↩] [↩]

- Statistics Canada. Skills in Canada: first results from the programme for the international assessment of adult competencies (PIAAC). 2013. https://www150.statcan.gc.ca/n1/en/catalogue/89-555-X2013001. [↩]

- J. Hussain, S. Salia, A. Karim. Is knowledge that powerful? Financial literacy and access to finance: an analysis of enterprises in the UK. Journal of Small Business and Enterprise Development. Vol. 25, pg. 985–1003, 2018, https://doi.org/10.1108/JSBED-01-2018-0021. [↩] [↩] [↩]

- Financial Consumer Agency of Canada. 2024 Canadian financial capability survey. 2025. https://publications.gc.ca/collections/collection_2025/acfc-fcac/FC5-42-1-2024-eng.pdf. [↩] [↩] [↩] [↩]

- Statistics Canada. Employment and unemployment rate, annual. 2025. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410037501. [↩] [↩] [↩]

- R. J. Oppenheimer. Indigenous and non-Indigenous 2021 unemployment, employment, and participation rates: improved from 2020—education is critical. Journal of Aboriginal Economic Development. Vol. 13, pg. 108–118, 2023, https://doi.org/10.54056/TJVT6073. [↩]

- Statistics Canada. The daily—pandemic benefits cushion losses for low income earners and narrow income inequality – after-tax income grows across Canada except in Alberta and Newfoundland and Labrador. 2022. https://www150.statcan.gc.ca/n1/daily-quotidien/220713/dq220713d-eng.htm. [↩] [↩] [↩]

- Statistics Canada. Profile table: Canada [country]. 2023. https://www12.statcan.gc.ca/census-recensement/2021/dp-pd/ipp-ppa/details/page.cfm?Lang=E&DGUID=2021A000011124&SearchText=Canada&HP=0&HH=0&GENDER=1&AGE=1&RESIDENCE=1&TABID=2. [↩]

- N. T. Luu, P. D. Hung. Loan default prediction using artificial intelligence for the borrow – lend collaboration. In Y. Luo (Ed.), Cooperative design, visualization, and engineering. Vol. 12983, pg. 256–270, Springer International Publishing, 2021, https://doi.org/10.1007/978-3-030-88207-5_26. [↩]

- S. Kremer, K. Mah. Improving financial literacy in Indigenous communities. 2021. https://www.canada.ca/en/financial-consumer-agency/programs/research/2021-building-better-financial-futures-challenge/improving-financial-literacy.html. [↩] [↩] [↩] [↩]

{kind=link}